Managing Power Demand In India

Q1. Could you start by giving us a brief overview of your professional background, particularly focusing on your expertise in the industry?

I am Dilip Joshi, with a BE (Mechanical), ME (Industrial Engineering), MBA (Finance), PGDIM, and more than 33 years and 6 months of experience in the power sector with Gujarat Energy Transmission Corporation Ltd (GETCO). I retired as Superintending Engineer from the State Load Despatch Center (SLDC), GETCO, Vadodara, Gujarat.

After retirement, I had worked as a sub consultant and carried out the following assignments/projects –

Technical Adviser, Wind, Solar, Demand forecasting at RE Connect Energy, Bangalore

Sub consultant with Idam infrastructure -projects of F&S, DSM, Ancillary services regulations, and the SAMAST project of the Forum of Regulators

Sub consultant as Solar expert for Ludhiana Smart City, Vizag Smart City, Aligarh Smart City, and Bihar Sheriff Smart City projects with AECOM

I have strong knowledge of solar and wind energy integration, energy storage, Smart Grid, and various power-sector-related regulations. I have been working as an Independent Director at an Ahmedabad-based solar company since July 2023 and have cleared the IICA exam for Independent Directors. I am providing freelance consultancy services for solar energy and power sector projects.

I had presented technical papers on Renewable Energy, Energy Storage, Distributed Generation, Geothermal Energy, Small hydro, and other power sector topics at various domestic (6 papers) and international conferences (9 papers).

Q2. The Ministry of Power has directed imported coal plants to run at full capacity from April 1, 2026, to meet the 270 GW peak summer demand. What does this move signal or what are your thoughts on this?

The Ministry of Power’s directive (issued around March 25, 2026) for imported coal-based (ICB) plants to run at full capacity from April 1 to June 30, 2026, signals an aggressive, proactive approach to avoid electricity shortages during an anticipated record-setting summer demand of over invoking Section 11 of the Electricity Act, the government is prioritizing supply security over cost, ensuring that industrial and residential needs are met during peak heat, even if it means importing more coal.

There are about 15 imported coal-based thermal power projects in India that have received this directive from the power ministry.

CGPL power plant -one of the biggest power plants

The 4000MW Mundra Ultra Mega Power Project (UMPP) in Kutch, Gujarat, is a coal-based thermal power plant with five 800 MW units providing electricity to Gujarat, Maharashtra, Rajasthan, Punjab, and Haryana

India has instructed Tata Power (NSE: TATAAPOWER) to run its 4-GW imported coal-based facility in Gujarat at maximum capacity between April 1 and June 30, as part of efforts to ensure sufficient electricity supply during the peak summer season, according to a government order seen by Reuters.

The company had suspended operations at all units of the Mundra plant on July 2, 2025, and has been suffering losses due to the temporary closure of the plant.

The directive emphasizes the need to step up generation from imported coal plants to meet rising demand during high-consumption months. Authorities have indicated that similar measures could be applied to other such facilities if required.

The decision comes against the backdrop of a projected surge in electricity demand, with peak consumption expected to reach around 270 GW in the coming months, compared with about 242 GW in 2025–26. The government aims to use idle or underused capacity to prevent supply shortfalls.

The move also follows the Gujarat government’s approval of revised power purchase terms with Tata Power, paving the way for the plant to resume long-term electricity supply.

The plant had remained largely non-operational for nearly six months due to high imported coal costs and the lack of a viable power purchase agreement.

To support operations, a government-appointed panel will set benchmark tariffs for power generated at the facility, providing clarity on pricing during the demand-intensive period.

The plant supplies 50% of the output to Gujarat. The company will subsequently ink a supplement PPA with Maharashtra, Rajasthan, Punjab, and Haryana.

Power Supply, Peak Demand And Availability Of Coal

There is sufficient power availability in the country. The present installed generation capacity of the country is 524 GW (as on 28th February 2026). The Government of India has addressed the critical issue of power deficiency by adding 299.87 GW of new generation capacity since April 2014, transforming the country from a power deficit to a power surplus.

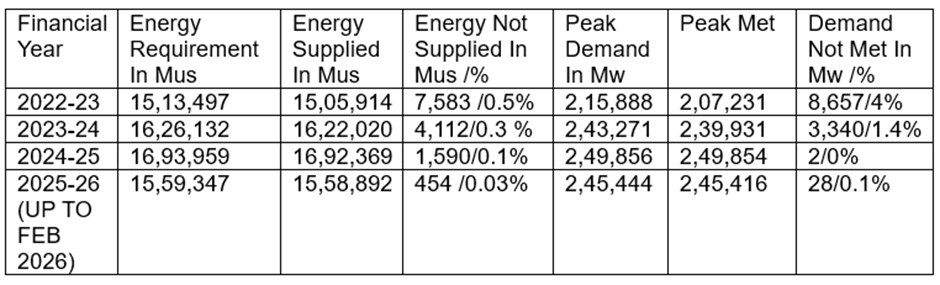

The country successfully met the all-time peak demand of 250 GW in the Financial Year (FY) 2024-25. The details of ‘Power Supply Position’ in terms of peak demand and energy requirement of the country for the last three FY and the current FY 2025-26 (up to February 2026)

The ‘energy supplied’ & ‘peak demand’ have been commensurate with the ‘energy requirement’ and ‘peak demand’, with only a marginal gap, which is generally on account of constraints in the State transmission / distribution network.

As on 22.03.2026, the coal stock available with coal-based plants in the country is around 58.2 million Tonnes (MTs), which is sufficient to run the plants for an average of 19 days at 85% Plant Load Factor (PLF).

Reasons for importing coal from Indonesia by IPP

Indonesian coal is generally superior to Indian coal, featuring a higher calorific value (5000–6500 kcal/kg) and low ash/sulfur content, making it cleaner and more efficient. Conversely, Indian coal is characterized by high ash content (often 30–40%+) and a lower calorific value, but is cheaper and offers greater supply security, often blended with Indonesian coal to improve utility performance.

Key Differences

Quality & Composition:

Indonesian Coal: Known for lower ash (<3% to 10%) and lower sulfur, leading to better combustion and reduced environmental impact.

Indian Coal: High ash content (average 30%–40%+) and higher moisture, resulting in lower energy efficiency and higher residue.

Calorific Value (Energy Content):

Indonesian Coal: Typically ranges from 3400 GAR to 6500 GAR, with 7000+ GAR coking coal available.

Indian Coal: Generally, lower calorific value, requiring more fuel to generate the same heat.

Cost & Availability:

Indonesian Coal: Higher upfront cost due to imports, but often more cost-effective due to higher energy efficiency.

Indian Coal: Cheaper base price but higher ash content requires more consumption, increasing operational costs.

Usage

Indonesian Coal: Ideal for power generation, cement manufacturing, and steel production due to high volatility and low sulfur.

Indian Coal: Primary fuel for domestic power plants, often blended with imported coal to balance high ash content.

In order to provide cheaper power to consumers, we need to reduce the power purchase cost and go for IPP. Many IPP companies had a Power

Purchase Agreement at a lower rate, considering cheaper coal from Indonesia. Indonesia initially provided/supplied coal at a lower rate, but once they understood their importance and demand, after some time, they also increased coal cost, so now it becomes difficult for IPP to meet the PPA rate, and since the PPA period is 25 yrs, they approached SERC and State Electricity companies to revise PPA rate , which was not possible as per terms and conditions of PPA. So IPPs have been operating their power plants for some time, and at last, SERC has to approve a revised PPA considering the rise in imported coal costs.

The Government of India has taken the following steps to meet the growing power demand in the coming years:

Generation and Storage Planning

- As per the National Electricity Plan (NEP), installed generation capacity in 2031-32 is likely to be 874 GW. With a view to ensuring generation capacity remains ahead of projected peak demand, all States, in consultation with the CEA, have prepared their “Resource Adequacy Plans (RAPs)”, which are dynamic 10-year rolling plans that include power generation and procurement planning.

- All the States were advised to initiate the process for creating/ contracting generation capacities from all generation sources, as per their

Resource Adequacy Plans.

- In order to augment the power generation capacity, the Government of India has initiated following capacity addition programme:

(A) The projected thermal (coal and lignite) capacity requirement by the year 2034–35 is estimated at approximately 3,07,000 MW as against the 2,11,855 MW installed capacity as on 31.03.2023. To meet this requirement, the Ministry of Power has envisaged setting up an additional minimum of 97,000 MW coal and lignite-based thermal capacity.

Further, the following initiatives have also been undertaken: -

Thermal capacities of around 18,160 MW have been commissioned since April 2023 till 31.01.2026. In addition, 38,745 MW of thermal capacity (including 4,845 MW of stressed thermal power projects) is currently under construction. The contracts of 22,920 MW have been awarded and are due for construction. Also, 24,020 MW of coal and lignite-based candidate capacity has been identified, which is at various stages of planning in the country.

(B) 12,723.50 MW of Hydro Electric Projects are under construction till 31.01.2026. Further, 4,274 MW of Hydro Electric Projects are at various stages of planning and are targeted for completion by 2031-32.

(C) 6,600 MW of Nuclear Capacity is under construction as of 31.01.2026 and is targeted for completion by 2029-30. 7,000 MW of Nuclear Capacity is under various stages of planning and approval.

(D) 1,54,830 MW Renewable Capacity, including 64,670 MW of Solar, 6,490 MW of Wind, and 59,990 MW Hybrid power, is under construction till 31.01.2026, while 47,920 MW of Renewable Capacity, including 35,440 MW of Solar and 10,080 MW Hybrid Power, is at various stages of planning and targeted to be completed by 2029-30.

(E) In energy storage systems, as of 31.01.2026, 13,120 MW / 78,720 MWh Pumped Storage Projects (PSPs) are under construction. Further, a total of 9,580 MW/57,480 MWh capacity of Pumped Storage Projects (PSPs) is concurred and yet to be taken up for construction. As of 31.01.2026, 10,658.94 MW / 28739.32 MWh Battery Energy Storage System (BESS) capacity is under construction, and 22,347.15 MW/ 69,836.70 MWh BESS capacity is under tendering stage.

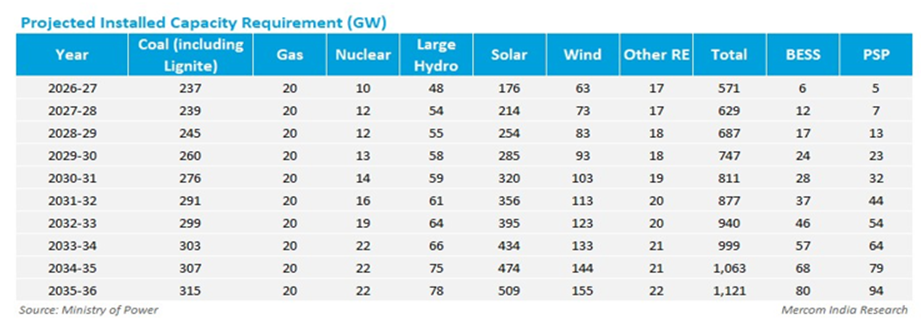

The CEA has projected that India’s installed power capacity requirement will reach 1121 GW by the financial year 2036, with the share of fossil fuel-based generation declining from the current 75% to 50%

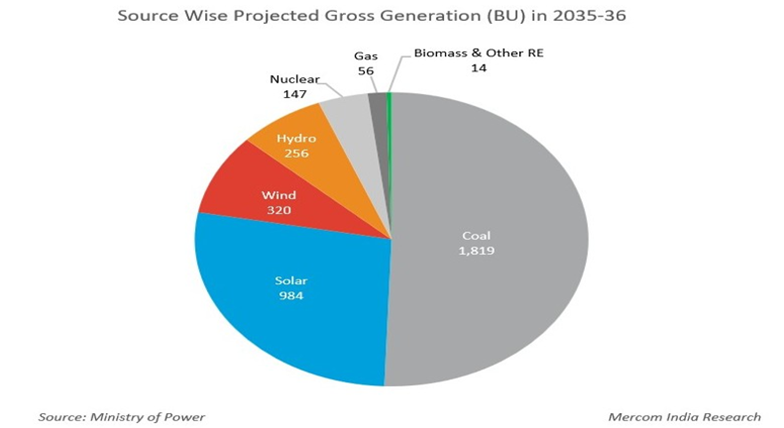

The CEA’s long-term national resource adequacy plan for FY 2027-2036 says coal will continue to serve as the backbone of the power system for base load supply, and solar, however, will account for the largest share of the installed capacity by FY 2036.

The projected installed power capacity requirement will comprise solar (509 GW), coal (316GW), Gas (20 GW), nuclear (22GW), large hydro (78 GW), small Hydro (6 GW), wind (155 GW), and biomass (16 GW)

CEA has projected a planning reserve margin of 13-14 % in FY 2036.

It has proposed adding 94 GW of Pumped Storage projects and 890 GW of battery storage systems (BESS) to enable flexibility in the use of renewables during periods of low renewable energy generation.

CEA said that integration of large-scale renewable and Energy storage capabilities would require parallel strengthening of the transmission network.

Transmission Planning

The Inter and Intra-State Transmission System has been planned, and its implementation is being taken up in a matching time frame with the addition of generation capacity. As per the National Electricity Plan, about 1,91,474 ckm of transmission lines and 1,274 GVA of transformation capacity are planned to be added (at a voltage level of 220 kV and above) during the ten-year period from 2022-23 to 2031-32.

In addition to the above, the Ministry of Power has issued guidelines dated 14.06.2024, 21.03.2025, and 15.12.2025 regarding the payment of compensation for Right of Way (ROW) for transmission lines, wherein the land rate is linked to the prevailing market rate. These guidelines address the key challenges in ROW arising from landowners demanding compensation above the rates set by the State Government.

Promotion of Renewable Energy Generation

- 100% Inter State Transmission System (ISTS) charges have been waived for inter-state sale of solar and wind power for projects to be commissioned by 30th June 2025 (with waiver tapering off 25% annually till June 2028), for co-located BESS projects commissioned by June 2028, for Hydro PSP projects where construction work awarded by June 2028, for Green Hydrogen Projects commissioned till December 2030 and for offshore wind projects commissioned till December 2032.

- Standard Bidding Guidelines for tariff-based competitive bidding process for procurement of Power from Grid Connected Solar, Wind, Wind-Solar Hybrid, and Firm & Dispatchable RE (FDRE) projects have been issued.

- Renewable Energy Implementing Agencies (REIAs) regularly invite bids for the procurement of RE power.

- Foreign Direct Investment (FDI) has been permitted up to 100 percent under the automatic route.

- To augment the transmission infrastructure needed for a steep RE trajectory, a transmission plan has been prepared till 2032.

- Laying of new intrastate transmission lines and creation of new substation capacity have been supported under the Green Energy Corridor Scheme for the evacuation of renewable power.

- A scheme to set up Solar Parks and Ultra Mega Solar Power projects is being implemented to provide land and transmission to RE developers for large-scale RE project installations.

- Schemes such as Pradhan Mantri Kisan Urja Surakshaevam Utthaan Mahabhiyan (PM-KUSUM), PM Surya Ghar Muft Bijli Yojana, National Programme on High Efficiency Solar PV Modules, New Solar Power Scheme (for Tribal and PVTG Habitations/Villages) under Pradhan Mantri Janjati Adivasi Nyaya Maha Abhiyan (PM JANMAN), and Dharti Aabha Janjatiya Gram Utkarsh Abhiyan (DA JGUA), National Green Hydrogen Mission, Viability Gap Funding (VGF) Scheme for Offshore Wind Energy Projects have been launched.

- To encourage RE consumption, the Renewable Purchase Obligation (RPO) followed by the Renewable Consumption Obligation (RCO) trajectory has been notified till 2029-30. The RCO, which is applicable to all designated consumers under the Energy Conservation Act, 2001, will attract penalties for non-compliance.

- “Strategy for Establishment of Offshore Wind Energy Projects” has been issued.

- Green Day Ahead Market (GDAM) and Green Term Ahead Market (GTAM) have been launched to facilitate the sale of Renewable Energy Power through exchanges.

- The Production-Linked Incentive (PLI) scheme has been launched to achieve the objective of localizing the supply chain for solar PV Modules.

Key Signals and Implications

Proactive Grid Security: The move indicates the government expects severe power demand surges (potentially exceeding the 2025 peak to secure supply, rather than reacting to shortages.

Prioritizing Reliability over Cost: Using imported coal is expensive. This decision highlights that the immediate priority is avoiding outages, especially as India experiences intense, extended summer heatwaves.

Strain on Domestic Infrastructure: This suggests that domestic coal supply, despite high production levels, may not be sufficient to meet absolute peak loads and industrial demand simultaneously.

Strategic Reliance on ICB: ICB plants, which can ramp up quickly, are essential for filling the gap between solar generation (which stops at night) and rising nighttime air conditioning loads.

My Thoughts on the Move

Necessary Temporary Measure: In the short term, this is a pragmatic move to manage the peak summer crisis, ensuring the economy doesn't suffer from power cuts.

Economic Impact: Reliance on imported coal could increase power generation costs, potentially putting pressure on DISCOMs (distribution companies) or leading to higher consumer tariffs.

Climate Concerns: While necessary, it highlights the continued reliance on fossil fuels during high-demand periods, presenting a challenge to India’s long-term sustainability goals.

Grid Stability: It reinforces the need for faster development of battery storage solutions and pumped hydro to replace this reliance on imported coal during peak hours in future summers.

Overall, this directive serves as a "bridge measure" to keep the lights on and fans running, balancing economic growth with grid stability amid extreme weather.

India's peak electricity demand is projected to grow rapidly from 277 GW in FY2026-27 to around 335 GW-388 GW by 2030, driven by industrialization, extreme heat, and electric vehicles. The power sector requires significant capacity expansion to manage this 5-year growth trajectory.

Peak Demand Projections and Key Trends (2026–2030)

FY2026-27: The 20th Electric Power Survey projects a peak demand of 277.2 GW.

2030 Demand: Projections indicate peak demand will exceed 335 GW, with some estimates reaching 388 GW.

Growth Drivers: The surge is fuelled by increased per-capita usage, rising temperatures requiring more cooling, rapid adoption of electric vehicles, and the growth of green hydrogen manufacturing.

Capacity Needs: To meet this demand, India must add substantial capacity, aiming for 500 GW of non-fossil fuel capacity by 2030, while strengthening its transmission network from 5 lakh ckm in 2026 to 6.48 lakh ckm by 2032.

Key Factors Influencing Future Demand

Rising Peak Variability: India is experiencing multiple demand peaks within a year due to extreme heat and cold, necessitating flexible power planning beyond just summer months.

Role of Conventional Power: Despite rapid growth in renewable energy, coal-based generation is expected to remain the backbone of India's power system for several years to meet base-load demand.

Sectoral Growth: The building sector, including residential and commercial units, is expected to drive the highest demand growth due to cooling needs.

Q3. With 40 million smart meters active as of April 2026, DISCOMs are moving toward Time-of-Day (ToD) tariffs. How does this shift affect the 'Payback Period' for a standalone solar project versus one with a 'Wind-Hybrid' component that can capture evening peak prices?

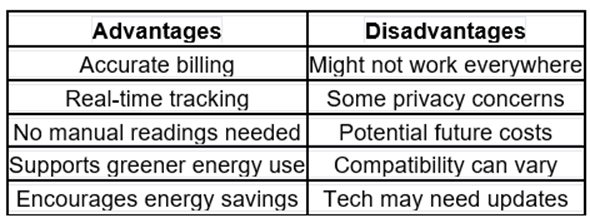

A smart meter is an advanced digital device that records electricity, gas, or water consumption in real time and securely communicates this data to utility providers for accurate, automated billing. They eliminate manual readings, allow for prepaid options, and help users monitor energy use via in-home displays or apps.

Key Benefits of Smart Meters

Accurate Billing & No Manual Readings: Smart meters automatically send usage data, eliminating estimated bills and manual meter readings.

Real-time Consumption Tracking: Consumers can use In-Home Displays (IHD) or apps to track energy usage, enabling them to understand, manage, and reduce energy consumption.

Lower Utility Bills: By identifying when they use the most energy, users can shift consumption to cheaper, off-peak times (e.g., overnight) and use energy-efficient appliances to save money.

Faster Fault Detection: Utilities can detect power outages and grid faults instantly, enabling faster, often remote, service restoration.

Prepaid Options: Similar to mobile phones, some smart meters offer rechargeable plans that help users track expenses in real time and avoid unexpected high bills.

Support for Green Energy: They facilitate the integration of renewable energy sources, such as solar panels, by accurately measuring both energy consumption and energy fed back into the grid.

Advantages and Disadvantages of Smart meters

As of April 2026, the widespread adoption of 40 million smart meters in India—enabling Time-of-Day (TOD) tariffs—fundamentally changes the economic valuation of solar projects. TOD tariffs make electricity 10%-20% cheaper during solar hours (9 am to 5 pm) and 10%-20% higher during evening peak hours (5 pm to 11 pm).

A Time of Day (TOD) electricity tariff is a pricing structure where electricity costs vary based on when it is consumed, designed to reduce grid load during high-demand periods. It features higher rates during peak hours and lower, cheaper rates during solar or off-peak hours.

Key Aspects of ToD Tariff in India

Structure: Typically divides the day into three, with 8 hours at lower "solar hours" rates and higher rates during evening "peak hours".

Solar Hours (Cheaper): Rates are generally 10–20% lower than normal tariffs during the daytime when solar energy is abundant.

Peak Hours (Expensive): Rates are 10–20% higher than the normal tariff, usually in the evening.

Implementation: Applicable to commercial/industrial consumers (10 kW+ demand) from April 1, 2024, and most other consumers from April 1, 2025.

Requirement: Requires a smart meter to measure electricity consumption at different times.

Benefits of ToD

Lower Bills: By shifting high-energy tasks (e.g., washing machine, dishwasher) to off-peak/daytime hours, consumers can save money.

Grid Stability: Encourages usage when solar energy is abundant, reducing the strain on the grid during peak evening hours.

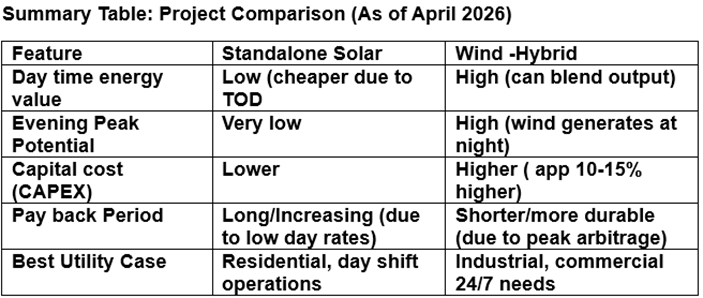

This shift significantly favors Wind-Hybrid projects over Standalone Solar projects, affecting their payback periods as follows:

Standalone Solar Project Payback Period

Impact: The payback period is longer or remains long for new standalone solar projects without existing, favorable long-term net metering agreements.

Mechanism: Because ToD lowers the value of power produced and consumed during the day (solar hours) and forces users to buy high-priced, non-solar power at night, the savings per unit decrease.

Limitation: The "duck curve" effect becomes sharper when solar generation is at its peak, the grid has a surplus, making the energy injected less valuable.

Result: In Maharashtra, for instance, limiting energy banking to same-time-slot adjustments means daytime generation cannot offset high-cost evening consumption.

Wind-Hybrid Project Payback Period

Impact: The payback period is shorter and more durable, especially for high-consumption industrial and commercial users.

Mechanism: Wind-hybrid systems produce power during the day (solar) and during high-potential times like the evening/monsoon (wind), allowing them to feed energy into the grid during the high-priced peak hours.

Advantage: While hybrid setups have higher initial capital costs, they provide 50–70% energy replacement, protecting users from high evening peak rates and high grid inflation, making them a more profitable long-term asset.

Result: Wind-solar hybrid projects, increasingly adopted, can offer a higher Capacity Utilization Factor (CUF) of 45-50% compared to ~20% for standalone solar, thereby maximizing savings during peak pricing periods.

In summary, the 2026 TOD regime penalizes daytime-only generation and rewards, through avoided high-peak costs, those with hybrid systems capable of shifting clean energy to the evening.

The shift to Time-of-Day (TOD) / Time-of-Use (TOU) tariffs fundamentally changes the question of when electricity is valuable—not just how much is generated. That directly impacts payback periods for different renewable configurations.

Let’s break this down analytically.

Impact of ToD tariffs in India

- Daytime (solar hours ~11am–5pm): discounted tariffs

- Evening peak (5pm–11pm): premium tariffs

- Smart meters enable granular billing and settlement.

Net effect:

- kWh is no longer equal in value

- Revenue depends on time-aligned generation

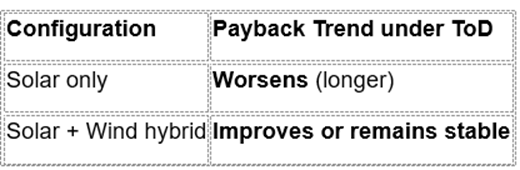

Standalone Solar: Payback Impact

Revenue profile

- It is generated mostly during low-price daytime

- Limited or zero output during peak-price evening

Consequences

Revenue compression

- Solar generation increasingly coincides with discounted tariff windows

- DISCOMs are actively incentivizing consumption during solar hours, not paying premium

Curtailment/lower marginal value

- High solar penetration → midday surplus → falling tariffs (or lower avoided cost)

Payback extension

Typical directional impact

- Pre-ToD payback: ~5–7 years (C&I rooftop in India)

- Post-ToD trend: +0.5 to 2 years longer payback (depending on tariff spread and net-metering rules)

Structural Advantage of Solar + Wind Hybrid in India

- Often peaks in late evening, night, and monsoon periods

- Has complementarity with solar

Key advantage under ToD

Ability to capture evening peak tariffs

Resulting economics

Higher weighted average tariff realization

- Solar-only: weighted toward discounted rates

- Hybrid: includes premium peak rates

Better capacity utilization

- More hours of generation → higher PLF

Reduced storage dependence

- Wind acts as a natural “virtual storage” substitute

Payback Comparison

Standalone Solar

- Revenue skewed to ₹ (low)

- Payback = slower

Solar + Wind Hybrid

Revenue mix:

- Day: RS (low)

- Evening: RS (high)

Blended tariff ↑ → cash flow ↑ → payback ↓

Typical directional difference

Delta:

Hybrid can improve payback by app 1–3 years vs standalone solar in strong ToD regimes

Key Drivers That Magnify This Gap

Peak tariff spread

Larger difference between day vs evening pricing → hybrid advantage increases

Wind resource quality

Strong evening/night wind → maximum benefit

Open access / C&I consumers

Direct exposure to ToD pricing → biggest impact

Storage cost

- If batteries are expensive → wind hybrid becomes even more attractive

Strategic Interpretation

Solar-only model is shifting from an energy generation asset → low-cost daytime energy asset.

The hybrid model becomes a time-arbitrage asset

Need an expert in this space?

Talk to an Industry Expert

Knowledge Ridge connects decision-makers with carefully vetted subject matter experts for one-on-one calls, research sprints, and advisory engagements — across 11 sectors and 163 sub-industries globally.

Comments

No comments yet. Be the first to comment!