Smart Capital In Renewables

Q1. Could you start by giving us a brief overview of your professional background, particularly focusing on your expertise in the industry?

I am Dilip Joshi, with a BE (Mechanical), ME (Industrial Engineering), MBA (Finance), PGDIM, and more than 33 years and 6 months of experience in the power sector with Gujarat Energy Transmission Corporation Ltd (GETCO). I retired as Superintending Engineer from the State Load Despatch Center (SLDC), GETCO, Vadodara, Gujarat.

After retirement, I had worked as a sub consultant and carried out the following assignments/projects –

• Technical Adviser, Wind, Solar, Demand forecasting at RE Connect Energy, Bangalore

• Sub consultant with Idam infrastructure -projects of F&S, DSM, Ancillary services regulations, and the SAMAST project of the Forum of Regulators

• Sub consultant as Solar expert for Ludhiana Smart City, Vizag Smart City, Aligarh Smart City, and Bihar Sheriff Smart City projects with AECOM

I have strong knowledge of solar and wind energy integration, energy storage, Smart Grid, and various power-sector-related regulations. I have been working as an Independent Director at an Ahmedabad-based solar company since July 2023 and have cleared the IICA exam for Independent Directors.I am providing freelance consultancy services for solar energy and power sector projects.

I had presented technical papers on Renewable Energy, Energy Storage, Distributed Generation, Geothermal Energy, Small hydro, and other power sector topics at various domestic (6 papers) and international conferences (9 papers).

Q2. With the ₹2.75 trillion investment opportunity in BESS by 2032, and Battery prices falling ~55% since 2024, at what specific 'discharge duration' should companies pivot from Lithium-Ion to Pumped Hydro Storage (PHS) in the current 2026 market?

Based on the rapid decline in lithium-ion battery costs—with pack prices dropping to $95/kWh in FY2025 and projected to fall further—combined with the massive deployment of 47 GW of BESS (Battery Energy Storage Systems) in India by 2032, the pivot point from Lithium-Ion to Pumped Hydro Storage (PHS) in 2026 has shifted significantly.

In the current 2026 market context, companies should pivot from Lithium-Ion to Pumped Hydro Storage (PHS) for discharge durations of 6 to 8 hours or more.

Key Market Dynamics

Li-ion Dominance (Short Duration): Due to the ~55% cost reduction since 2024 and falling LCOS (Levelized Cost of Storage), Li-ion is the dominant choice for 1–4-hour applications (ancillary services, renewable balancing, peaking capacity).

PHS Superiority (Long Duration): For energy storage lasting 6+ hours, PHS offers better economics, as the cost of scaling battery capacity (MWh) linearly increases, while PHS projects can store large amounts of energy at a lower marginal cost per unit for extended periods.

Specific Pivot Factors for 2026

6–8+ Hours Pivot: While BESS is becoming competitive for 4-hour systems, 8-hour or multi-day storage required for grid-scale firming still heavily favors PHS, which is better suited for long-duration applications (6–12+ hours).

VGF Support: The Indian government's VGF (Viability Gap Funding) program specifically targets 13.2 GWh of battery projects, reinforcing that 2–4-hour storage is the current sweet spot for, often with a 2-hour minimum required in solar tenders.

Projected Trends: By 2030, while BESS costs are expected to drop to $68/kWh, PHS will remain the preferred technology for long-duration and inter-day energy shifting, rather than intraday balancing.

The pivot point is no longer a fixed number like “4 hours”—it has shifted materially by 2026 due to falling Li-ion costs (~50–60% drop) and evolving revenue stacks (ToD arbitrage, capacity payments, ancillary stacking).

Where the physics & market naturally divide

Across sources, the technology envelope today looks like this:

Li-ion BESS: 1–4 hrs (core), now stretching to 6 hrs economically

Pumped Hydro (PHS): typically, 6–24+ hrs

India-specific planning also aligns with this:

BESS → generally up to 4 hours.

PHS → more than 6 hours

So historically, the crossover band = ~4–6 hours

2026 reality: cost compression has shifted the crossover

Recent analysis shows:

BESS now:

- Competitive at ~6 hrs

- Approaching viability at 8–10 hrs

But:

- Cost per stored kWh still scales linearly for Li-ion (more batteries needed)

- PHS cost per kWh is structurally lower for long duration

Meaning

- The technical boundary hasn’t changed

- The economic boundary has moved upward

The real “pivot duration” in 2026

In the 2026 Indian market, the rational pivot is: ~7–8 hours discharge duration, because:

Below ~6 hrs → Li-ion dominates on:

- Capex speed

- TOD arbitrage frequency

- 85–90% efficiency

Above ~8 hrs → PHS dominates on:

- RS/kWh capex (3–4× cheaper energy capacity)

- 50–80-year life vs 10–15 yrs (battery replacement risk)

- Better suited for multi-cycle + seasonal shifting

Between 6–8 hrs → depends on:

- Land availability (PHS constraint)

- Revenue stacking (capacity payments vs arbitrage)

- Hybridization (solar + wind + storage)

Why does this matter more under TOD tariffs

With TOD pricing

- Solar-only arbitrage window = 4–5 hrs (day → evening)

- Wind + solar hybrid extends to 6–8 hrs

That’s the key insight:

- Standalone solar + BESS → stays <6 hrs → Li-ion wins

- Wind-hybrid or RTC contracts → push toward 8+ hrs → PHS starts winning

Strategic takeaway

By 2026–2030, portfolios are splitting:

BESS focus

- 2–6 hr systems

- Urban / substation / congestion nodes

- High cycling (1–2 cycles/day)

PHS focus

- 8–16 hr systems

- RTC / firm RE supply

- Capacity payments + long-duration arbitrage

Hybrid sweet spot

- Solar + Wind + 6–8 hr BESS initially

- Transition to PHS as the duration requirement grows

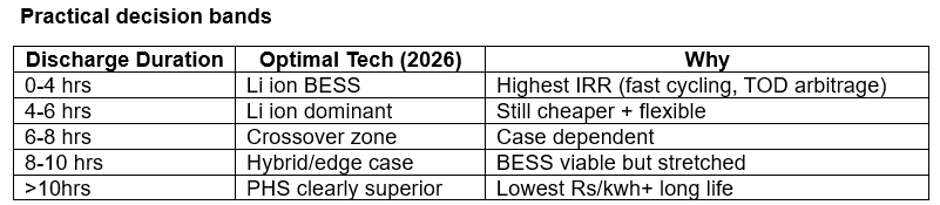

Companies should pivot from Li-ion to Pumped Hydro at ~7–8 hours of discharge duration in the 2026 market.

<6 hrs: Li-ion unequivocally superior

6–8 hrs: economic crossover (case-specific)

>8 hrs: PHS structurally advantaged

For daily, high-frequency balancing in 2026, Lithium-ion remains superior; however, for overnight or multi-day firming of renewable energy, companies should pivot to PHS to avoid the high costs of long-duration battery storage.

Though the cost of battery is high at present, much research is going on for various types of batteries, and all are trying to reduce the cost and increase the life of the battery. So, in the near future, the cost of batteries will be more realistic/economical. There are other ESS technologies such as Compressed air storage systems, Gravity model, thermal storage, etc., but they are not used -it's costly and at the developing stage.

Q3. From a Grid Connectivity standpoint, is it more financially viable in 2026 to 'Repower' old wind sites with modern high-efficiency turbines?

From a Grid Connectivity standpoint, repowering old wind sites with modern turbines is highly financially viable and, in many cases, superior to new greenfield developments in 2026. While grid congestion remains a bottleneck in 2026, repowering leverages existing infrastructure—land rights, permitting, and grid connections—which reduces development risks and timelines.

Replacing old windmills with higher-capacity, modern turbines—known as repowering—offers greater efficiency but poses significant challenges. Key issues include high capital costs, complex logistics for transporting massive blades, the necessity for more land, waste management of old blades, fragmented ownership of existing sites, and long-term Power Purchase Agreements (PPAs).

Key Issues in Repowering Wind Projects

Financial & Economic Hurdles: Repowering is expensive. Without incentives, it is often seen as uneconomical, especially when replacing smaller, functional units. Furthermore, new installations often lose existing incentives (such as banking facilities) and are treated as new projects, thereby impacting profitability.

Logistics and Infrastructure: New, higher-capacity turbines are significantly taller and larger, making transportation from factories to sites a massive logistics challenge. Existing roads and infrastructure may not support the transportation of large components.

Land Use and Ownership: New, larger turbines require more space (roughly 3.5–5 acres per turbine). Fragmented ownership of the old, small turbine sites often leads to disputes and delays.

Ownership issues

In India, there are pooling stations with multiple windmills owned by various CPPs/industries to meet their own power requirements /set up in their light bills. These CPP/wind owners may not agree to replace their windmill or invest in a new one.

Environmental & Disposal Issues: Dismantling old turbines leaves behind massive amounts of composite material—such as fiberglass—which is difficult to recycle, creating waste management challenges.

Operational Challenges: Increased hub heights and larger rotor diameters require improved grid infrastructure, transmission systems, and grid stability management to handle the higher capacity.

Technological Shift: The transition involves advanced technology (such as removing gearboxes) that requires specialized expertise and maintenance, with less historical performance data available compared to older models.

Environmental Impact Studies: Since wind sites were first developed, local habitats may have changed, creating new challenges for planning permissions.

Environmental Issues: Many old turbines have gearboxes with oils that can leak. The disposal of the huge, durable, but non-recyclable turbine blades—43 million tons anticipated by 2050—presents a major, unresolved environmental challenge.

Key factors driving the financial and technical viability of repowering in 2026 include:

Grid Capacity Utilization: Repowering optimizes already connected, high-quality wind sites, which is more attractive than facing long queues and massive costs for new grid interconnections.

Increased Output, Same Infrastructure: Modern, taller turbines can triple or quadruple power production from the same site while using existing, already-approved transmission lines, often without requiring major upgrades.

Optimal Resource Usage: Old, sub-1-MW turbines (often installed in the 1990s) occupy prime locations. Replacing them with 3-5 MW+ turbines at these sites ensures the best wind resources are exploited without the challenges of land acquisition.

Reduced Development Risk: Repowering avoids many of the regulatory hurdles (permitting) that can take years for new projects, offering faster deployment times in a high-cost environment.

Lower Levelized Cost of Energy (LCOE): While upfront capital costs are high, the significantly higher capacity factor (often doubling output) results in a better long-term return on investment (ROI) than building new projects in suboptimal, remote locations.

However, the viability is subject to regional regulations. In some regions, grid operators may permit replacing multiple old, small turbines with a single large turbine, but may restrict the total capacity to the original PPA level, which can complicate the business case for adding more power. Nonetheless, with 2026 seeing stabilized turbine costs, repowering is often an "easy economic decision," particularly for sites older than 12-15 years.

Short answer: Yes—from a grid connectivity standpoint, repowering old wind sites is often more financially viable in 2026—but only under specific conditions.

The key is that grid economics—not turbine CAPEX—is now the dominant driver.

Repowering leverages:

- Existing evacuation lines, substations, and land rights

- Avoids new transmission build (which is now a major bottleneck in India)

This is critical because:

- New RE projects increasingly face grid congestion + delayed connectivity

- Transmission upgrades are capital-intensive and time-consuming

Financial Impact of Repowering

Avoided grid capex (biggest lever)

For Greenfield wind

- 15–25% of the project cost can be for evacuation + connectivity infra

For repowering

- Much of this is already sunk

- Incremental upgrades only (not full build)

Result

₹0.3–0.6 Cr/MW effective saving (typical industry range)

Faster project execution → IRR boost

- No land acquisition delays

- No right-of-way issues

- Faster approvals (increasingly policy-supported)

Example

Gujarat policy gives priority connectivity + transmission waivers

Faster COD = higher IRR by ~1.5–3%

Higher generation from the same grid node

- Old turbines: ~10–14% CUF

- New turbines: ~25–35% CUF

Repowering can

- Increase output 1.5× to 2× minimum

- Even boost capacity factors ~80% nationally

Repowering is not always financially superior due to grid constraints.

Legacy grid incompatibility

Many old sites

- Designed for 0.2–0.6 MW turbines

- Use 11 kV feeders

Modern turbines

- 2–4 MW → higher current loads

Leads to:

- Transformer overload

- Voltage instability

- Need for 33 kV+ upgrades

This can erode the cost advantage.

Connectivity rights & ownership fragmentation

- Multiple turbine owners on the same site

- Shared evacuation infrastructure

Makes:

- Grid access restructuring complex

- Financing harder

Tariff lock-in problem

- Old PPAs (₹4–5/kWh) vs new bids (~₹3/kWh)

Developers sometimes

- Prefer to keep old turbines running

- Instead of repowering

Repowering wins financially + grid-wise when:

Ideal conditions

- High wind resource site (Class I zones)

- The existing grid has headroom or upgradeable capacity

- Single / consolidated ownership

- Access to new PPA or merchant/RTC market

In these cases repowering is one of the cheapest ways to add new generation capacity in India today

When Greenfield is still better when:

- The old grid is too weak / expensive to upgrade

- The site has fragmented ownership

- Developer wants hybrid (solar + wind + storage) integration

- New location has better wind + transmission corridor (ISTS)

Q4. Given the current global supply chain for CRGO steel and the domestic surge in transformer demand, what is the 'true' lead time you are seeing on the ground for 765kV equipment?

Based on the current 2026 market landscape, the "true" on-the-ground lead times for 765kV transformers are commonly 24 to 36 months, with some maximums reaching 60 months in extreme cases, exacerbated by chronic shortages of CRGO steel.

In India, where domestic demand for 765kV equipment is experiencing a massive surge, PGCIL (Power Grid Corporation of India Limited) has seen delivery timelines for high-capacity transformers stretch to 20–24 months.

Supply chain drivers impacting these timelines:

The 'True' Lead Times

765kV Transformers: While some suppliers argue 12–14 months is possible after engineering drawing approval, the industry standard for new, large 765kV power transformers is currently 24–36 months.

Components Bottlenecks: A transformer built only moves as fast as its slowest component. High-voltage bushings and on-load tap changers (OLTCs) are causing severe bottlenecks.

Turnkey Projects: Comprehensive projects, including 765/400kV substation upgrades, often have commissioning schedules of 30 months.

CRGO Steel Constraints

Import Reliance: India relies heavily on imports for Cold-Rolled Grain-Oriented (CRGO) steel, with domestic production meeting only about 10-12% of demand.

Supply Shortage: A reported 30% shortage of CRGO steel is impacting the industry, largely due to uncertainty in import licenses from Japan, South Korea, and China.

Increased Pricing: The shortage has driven up prices, impacting smaller manufacturers, though large players are prioritizing supply for 765kV projects.

Domestic Surge Drivers

Power Grid Expansion: 765kV networks are expanding rapidly, now comprising roughly 11.5% of the high-voltage network as of early 2026.

Bulk Tenders: Major orders are being placed for 765kV transformers to support renewable energy integration and grid stability, often in bulk lots

Government Initiatives: High government-driven spending on UDAY and transmission expansion is driving demand for higher voltage transformers

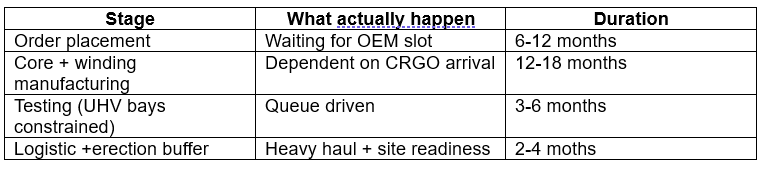

Real execution sequence

Need an expert in this space?

Talk to an Industry Expert

Knowledge Ridge connects decision-makers with carefully vetted subject matter experts for one-on-one calls, research sprints, and advisory engagements — across 11 sectors and 163 sub-industries globally.

Comments

No comments yet. Be the first to comment!