AI Infrastructure: Hype or Horizon?

Q1. Which technology transformation programs have you been directly accountable for, and what business outcomes or investment decisions ultimately defined their success?

Sixteen years in, the programs I'm most proud of aren't the ones with the biggest budget; they're the ones where architecture genuinely moved a business decision.

I've led transformation initiatives across IoT, cloud-native, and AI/ML platforms for energy and industrial clients in the US, the UK, Europe, Japan, and South Korea. But the moments that defined success were specific. One program I led directly informed a multi-million-dollar asset modernization investment for a Fortune 500 energy client; the business case was built on predictive maintenance savings and operational risk reduction that my architecture work uncovered.

Another was replacing legacy SCADA integrations with a cloud-native data platform that reduced time-to-insight from days to minutes, changing how procurement and scheduling decisions were made downstream.

What I've learned is that transformation programs succeed when Enterprise Architecture stops being a governance function and starts being the bridge between technology options and investment-grade decisions. That shift in positioning changes everything.

Q2. What structural shifts are driving the current wave of investment in AI data centers, and how sustainable do you believe this growth trajectory is over the long term?

The demand is real, but I'd separate the structural from the speculative, because they're getting bundled together in a way that concerns me. The genuine structural driver is inference at scale. Training frontier models needs massive GPU clusters, yes, but that's a finite event. What sustains demand over the long run is AI moving from experimentation into production workloads embedded in enterprise systems, industrial operations, and customer applications. That inference layer is durable.

What worries me is the portion of the investment that's outpacing actual enterprise adoption. A lot of capacity is being built on the assumption that demand will catch up. In my experience working with large enterprises, the journey from AI pilot to production deployment is harder and slower than most investment models assume.

My honest view: this wave will consolidate. The infrastructure built for real, production-grade workloads will generate strong returns. The rest will face a reckoning when adoption timelines stretch.

Q3. How is the rise of AI-native infrastructure changing traditional approaches to data center architecture and design?

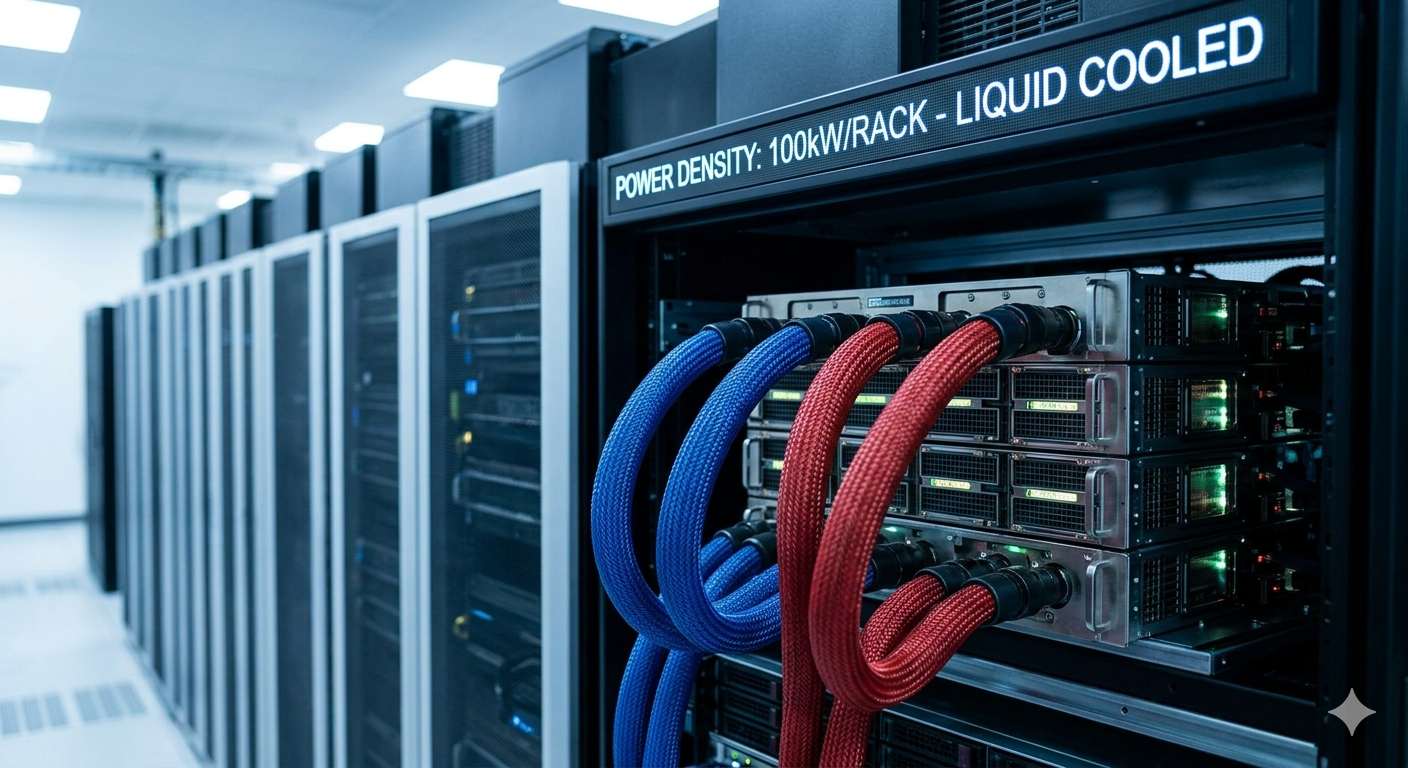

Traditional data centers were designed around predictable workloads and stable power. AI breaks both of those assumptions, and the rethink required is more fundamental than most people realize.

The most visible change is in power density. We've moved from 5-10kW per rack to 40–80kW and beyond in serious AI deployments. That forces a complete redesign of cooling, power distribution, and physical layout, not an incremental upgrade.

The compute fabric has changed, too. GPU clusters with high-bandwidth interconnects demand architectural patterns that legacy infrastructure simply wasn't built for. And the software and orchestration layer has to support dynamic resource allocation, high-throughput storage, and low-latency networking at a scale that older design patterns can't accommodate.

What I find most interesting from an Enterprise Architecture lens is the edge dimension. AI inference is increasingly being pushed toward the data source — industrial sites, substations, remote assets. So data center architecture today has to account for a distributed edge-to-cloud continuum, not just a centralized facility. That's a genuinely different design problem.

Q4. Do you see sustainability becoming a genuine differentiator in the AI data center market, or will it increasingly become a baseline requirement?

Differentiator today, baseline within three to five years, that's my read.

Right now, energy efficiency and renewable sourcing genuinely influence procurement decisions, especially among large enterprises with their own net-zero commitments. So there's real commercial value in credible sustainability credentials at the moment.

But the direction of travel is clear. Regulatory pressure is building, carbon reporting is tightening, and energy costs are becoming a competitive variable rather than just an operational one. When that happens, sustainability stops being a selling point and becomes the price of entry.

What I think is underappreciated in this conversation is the second-order pressure. AI data centers are among the most energy-hungry assets being built right now. In a market like India, where the renewable mix is still developing, how a facility is powered will directly shape where it gets built and at what scale.

So sustainability isn't just an ESG story. It's becoming a core constraint in infrastructure planning, and the operators who recognized this early are quietly building a structural advantage.

Q5. How is India's position within the global AI infrastructure ecosystem evolving, and what factors are shaping its competitiveness?

India's position has genuinely shifted, and I say that having watched this space closely for years, not just as a talking point.

The IndiaAI Mission, the semiconductor policy push, and the hyperscaler commitments landing in Mumbai, Chennai, Hyderabad, and Pune are real signals. They reflect a convergence of government intent, enterprise demand, and deep technology talent that's hard to replicate quickly elsewhere.

What excites me is the possibility of India moving beyond hosting compute capacity to actually contributing to AI development - sovereign models, local data assets, indigenous capability. That's a different and more valuable position in the global ecosystem.

But I watch one constraint above everything else: power. Data center growth in India will ultimately be governed by a reliable, affordable, and increasingly green power supply. That's not a future problem - it's already shaping site selection decisions today. How India solves that infrastructure challenge will determine whether it becomes genuinely competitive with Southeast Asia and the Middle East, or remains a promising market with a ceiling.

Q6. What assumptions underpinning current AI data center investment strategies deserve the greatest scrutiny?

The one I'd push hardest on is the assumption that enterprise AI adoption will scale smoothly into production workloads within the timelines most investment models use.

In my experience working with Fortune 500 clients across the energy and industrial sectors, the gap between a successful AI pilot and enterprise-scale deployment is wider than it appears from the outside. Data readiness, integration complexity, and the organizational change required to actually use AI outputs - these are real friction points that don't show up cleanly in demand forecasts.

I'd also scrutinize the assumption about energy availability. Infrastructure plans are being drawn up in markets where grid capacity and renewable supply cannot be guaranteed to keep pace.

And there's a third one that doesn't get enough attention: model efficiency. If AI continues to get more efficient - requiring less compute per unit of useful output - the demand curve changes materially. That's not a fringe scenario; it's already happening. Investment strategies that treat current GPU demand as a stable baseline may be modeling a world that shifts beneath them.

Q7. If you were advising policymakers on building a globally competitive AI infrastructure ecosystem, which priorities would you consider most critical and why?

The first thing I'd say is: don't lead with compute. The countries that are winning in AI infrastructure invested in enabling infrastructure first - reliable power, high-capacity connectivity, and land with the right conditions for large-scale development. Data centers don't work without those foundations, and chasing capacity before solving for them is a mistake.

Second, distinguish between hosting compute and building capability. Attracting a hyperscaler is a start, but it doesn't compound over time the way sovereign AI capability does. The nations that will matter in the long run are investing in domestic model development, local data assets, and regulatory environments that allow responsible deployment at scale.

Third - and I feel strongly about this - treat talent as infrastructure. The constraint on AI competitiveness is often the availability of deep AI and data engineering expertise as much as it is hardware or bandwidth.

The overarching point I'd make to any policymaker is this: AI infrastructure competitiveness isn't won through a single policy lever. It requires a coordinated architecture - energy, connectivity, talent, regulation, capital - that holds together over a sustained horizon. Fragmented interventions rarely compound.

Need an expert in this space?

Talk to an Industry Expert

Knowledge Ridge connects decision-makers with carefully vetted subject matter experts for one-on-one calls, research sprints, and advisory engagements — across 11 sectors and 163 sub-industries globally.

Comments

No comments yet. Be the first to comment!