An Introduction To LNG Fuel Pricing

Introduction

Procuring LNG fuel usually means taking out a term contract, typically for one to five years. Increasing competitiveness in more mature ports and regions, such as the Amsterdam-Rotterdam-Antwerp (ARA) ports area and the Baltic, is leading to a shortening in the duration of term contracts. In these locations we are seeing the emergence of more flexible and short-term trades. These include ’spot’ bunkers traded a couple of weeks or even days ahead of delivery. Most LNG bunker volume is contracted on long-term contracts, however.

Within term contracts – and similarly to pipeline gas sales – LNG fuel prices are typically either gas-indexed or oil-indexed. This means they escalate in line with either gas prices quoted by hubs such as the Netherlands’ Title Transfer Facility (TTF), or with Brent crude oil or gasoil quotes. However, for short-term or occasional bunker trades, the LNG fuel price can be fixed, i.e., it is independent of future developments in gas or oil prices. Simplified, price escalations follow this structure:

LNG price = Alpha * Index + Add-on,

Like traditional bunker fuels, LNG fuel price structures can be split between a commodity component (the LNG market value) and a logistic component, which is the cost of delivery including shipping to the bunkering location. Simplified, the Alpha * Index element reflects the commodity component, while the logistic component is reflected by the Add-on element. Index may refer to a gas benchmark; typically, the TTF, the Henry Hub (HH), the Platts LNG Japan Korea Marker (JKMTM) or the UK National Balance Point (NBP). Or it may refer to an oil-related benchmark (Brent, gasoil, heavy fuel oil). In the case of fixed prices, the firm quotes offered reflect the forward value of above price escalations for the delivery period.

In contrast to fuel oils, LNG fuel prices are often expressed by energy content, with units depending on the market (location). Prices in Continental Europe and UK are typically expressed per megawatt hour (MWh) and per them respectively, while US and other markets use million British thermal units (MMBtu). When prices are quoted per metric ton, buyers should be careful to establish if this is tons LNG or tons fuel equivalents. Furthermore, buyers should be aware if prices are quoted based on either a gross calorific value (GCV) or net calorific value (NCV). Giving prices based on GCV, or higher heating value (HHV), is the most common practice in the global gas and LNG industry. The GCV/NCV ratio for LNG is 1.108, often rounded to 1.11.

Gas-indexed pricing

Gas-indexed LNG fuel prices generally follow a rather transparent price escalation, and the following gas-indices serve as the basis: TTFEUR/MWh (Continental Europe); HHUSD/MMBtu (Global, incl. Western Europe); and, JKMUSD/MMBtu (Asia) and NBPGBP/them (UK).

While gas-indexed price escalations typically are quite simple, there are some elements that differ between the suppliers, including the index definitions. The most common indexations for physical delivery are referred to as day-ahead (spot) and month-ahead (front-month). Within TTF, the most common index definitions are monthly average of month-ahead quotes (TTFMA average), monthly average of day-ahead quotes (TTFDA average) and single day-ahead quotes of the day before the bunkering (TTFspot or TTFDA). TTFMA average has been the most attractive indexation for both buyers and suppliers, as it removes the risk of extreme spot prices and simplifies invoicing as the monthly price is fixed on the first day each month. However, as the practice is very similar to conventional bunker fuels, the TTFspot (TTFDA) is becoming more widespread for ship-to-ship LNG bunkering.

The benchmark price source used to create the indices can also differ between suppliers. Exchanges (e.g., ICE Endex and PEGAS) can publish the indices directly, usually as a volume-weighted average of daily trades, or indirectly by publishing settlement quotes or bid/ask prices. In the latter case, suppliers can calculate the indices themselves, though these will not be volume weighted. As a supplement or alternative to the exchange-sourced indices, independent price-reporting agencies (e.g., Argus, ICIS Heren, and S&P Global Platts) publish price benchmarks for physical trading.

Whether quoted prices are based on GCV or NCV may also differ between suppliers.

Gas indexations usually facilitate transparency for each element of the value chain. In the simplest and most transparent form, prices are provided per energy unit based on NCV, and the price escalation follows this equation:

LNG bunker price = 1.11 * TTFMA + fee

Here, 1.11 is the factor converting the TTF index from GCV to NCV. Some suppliers are more precise and use 1.108, while some use normative GCV and NCV values to create the factor. The TTFMA is either a benchmark index published by Argus, ICIS Heren or Platts, or an index published by ICE Endex or EEX’s PEGAS platform. The fee is given per energy unit, and represents the logistics costs and service charge, covering reloading, distribution, fuel consumption and bunkering. It also includes the suppliers’ margin.

While the previous price escalation example is based on NCV, our impression is that pricing based on GCV is more common. In this case, the prices are not directly comparable with conventional fuels, which are normally given based on lower heating value. Price escalations typically follow the following generalized equation:

LNG bunker price = alpha * TTF index + fee

Alpha is a factor typically ranging between 1.03 and 1.15, assumed to include the supplier’s trade margin (LNG commodity margin), and sometimes the fuel cost (boil-off gas). TTF index can be both day-ahead and month-ahead. The fee is given per energy unit and, as in the previous example, represents logistics costs and the service charge. The fee typically depends, among other variables, on the location (distance from source) and mode of bunkering (ship-to-ship, truck-to-ship, etc.).

In some cases, the seller and buyer agree to invoice and pay logistics costs on, or close to, a pass-through basis. In these cases, the buyer may have higher expectations of price transparency, leading to bespoke price formulas. An example could be the following:

LNG bunker price = Alpha * TTF index + terminal loading cost + port dues + distribution (e.g. trucking costs or time charter rate, and fuel costs/boil-off gas) + service charge

In addition to the introduced components of gas-indexed LNG price escalations, several other elements should be accounted for depending on numerous factors. For example, when HH-indexed LNG bunker is delivered in Western European ports, the EUR/USD exchange rate is added to the formula. This is because the commodity is sold in EUR while the index is given in USD. There are also cases where the LNG is sold in EUR or GBP, but the logistics cost is based on the time charter rate of the LNG bunker vessel and paid in USD. Also, if the term contract spans multiple years (> 2 years), it is common to peg the logistics cost either to the consumer price index (CPI), or to labour costs (local indexes).

Although the LNG bunker price is usually a variable unit price per energy quantity delivered, there are some cases where lump-sums are added on an operation-by-operation basis, independent of the volume bunkered.

Oil-indexed pricing

For oil-indexed pricing, it is common practice to escalate on the Brent crude oil index, as these exposures are easy to hedge financially. In that case, price escalations follow this structure:

LNG price [currency/unit] = Alpha [%] * Brent [USD/bbl] + Add-on [currency/unit] * CPI

Alpha is referred to as the ‘slope’ and sets the commodity price level against Brent crude oil quotes. At the statistical energy content of 5.8 MMBtu per barrel oil equivalent, a slope of 17.2% (1/5.8) is considered to be the ‘gas-to-oil parity’. This implies, for example, that a 12% slope translates to an LNG discount of 30% (12/17.2 = 0.7) compared with oil equivalents, excluding logistics costs. Add-on reflects supply chain and logistics costs. The supplier’s gross margin is typically less transparent, as it is included in the slope and/or in the add-on premium. On the other hand, an oil-indexed price will often offer a more predictable return on investment than a gas-indexed price.

As an alternative to Brent crude oil indexation, some buyers prefer gasoil-related indexation as this regulation guarantees a discount against the distillate fuel alternatives (marine gasoil, marine diesel oil). Price escalations follow this structure:

LNG price [currency/unit] = Coefficient * Gasoil [USD/ton] + Add-on [currency/unit] * CPI

Coefficient combines both a discount slope against oil equivalents and a gasoil calorific value adjustment. For example, if the gross calorific value of gasoil is 12.65 MWh/ton and the LNG commodity (excluding logistic costs etc.) is sold with a 30% discount, the coefficient should be 0.0553 (0.7/12.65).

Gasoil represents a benchmark contract and may vary according to region. Gasoil 0.1% FOB ARA (free on board in the ARA area) is most used in Northwestern Europe. Gasoil 0.1% CIF MED (cost, insurance and freight in the Mediterranean) is most commonly used in the Mediterranean Sea basin. Add-on represents logistics and supply chain costs, and in practice the coefficient is usually fixed after these are known, to try to offer an overall competitive price.

For both Brent- and Gasoil-indexed LNG prices, exchange rate factors are added to the formulas when LNG prices are not given in USD.

Conclusions

For many years, natural gas – both piped and LNG – was typically sold under long-term contracts with prices regularly adjusted and indexed to market prices of so-called competing forms of energy. While these competing energy forms have included electricity, coal and even firewood, a substantial component of the long-term gas price indexation has been based on market prices of either crude oil or oil-derived products such as home heating oil and heavy fuel oil.

For a number of reasons, the last two decades have seen incrementally rapid changes to this conventional situation. First, an increasing number of gas production and transport projects are no longer underpinned by long-term sales contracts at all – or even where a contract is in place, the term may be 10 or 15 years as compared with the 25 or 30 years typically seen in the past. Secondly, the emergence of liquid gas markets, often based around natural gas hubs (Henry-Hub, TTF, NBP), has increasingly challenged the idea that natural gas should be valued solely by reference to competing (different) energy forms (ex. JKM) and has no inherent value of its own. And finally, the structure of energy markets and energy consumption patterns has evolved to the point that oil-based products are no longer the only, or even the most substantial, competitor to natural gas as an energy source.

This last trend has no doubt been motivated in the first instance by emerging sensitivities to climate change, greenhouse gas emissions and other negative environmental consequences of oil consumption. This in turn has powered the spectacularly rapid development of cost-effective renewable energy technology, to the point that in many countries solar and wind power can – without government intervention – compete effectively with fossil-generated power from a cost viewpoint. Faced with these potentially threatening developments, major actors – commercial, governmental and NGO – in the natural gas sector are seeking to ‘green’, or gain environmental credibility for, their projects. This tendency is particularly marked in the LNG sector, where in recent years several LNG projects, contracts and deliveries have been certified green or carbon-neutral either only on their upstream portion or their entire life-cycle.

Recent developments in LNG markets, include attempts to create a proper gas-to-gas competition delinked from oil amid the perception of the oil price as a stabilizing mechanism, that have occurred particularly during periods of gas oversupply. While new challenges to LNG markets include the emergence of green LNG and the underlying need to change the related pricing mechanisms.

Annexes

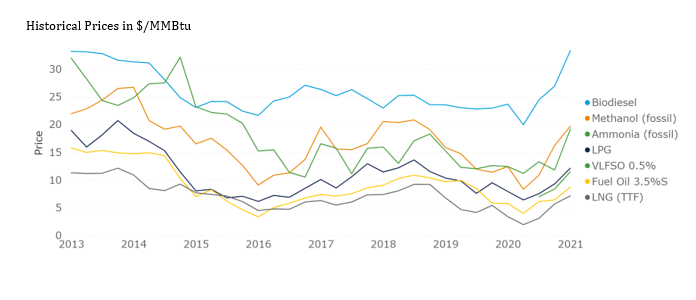

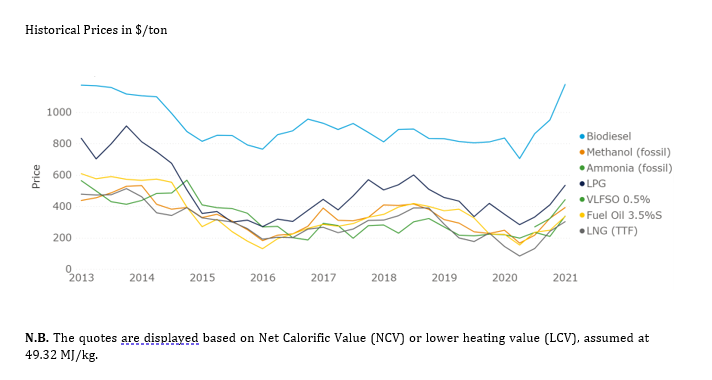

N.B. The quotes are displayed based on Net Calorific Value (NCV) or lower heating value (LCV), assumed at 49.32 MJ/kg.

LNG (TTF) means the TTF Front Month: Launched in 2003, the TTF (Title Transfer Facility) is the Dutch natural gas market. As the biggest and one of the most established gas markets in Europe, it is now the benchmark for price formation across the entire continent, not only for natural gas but also increasingly for liquefied natural gas (LNG).

Although a waning producer of natural gas and with only limited demand relative to larger neighbours like the UK and Germany, the Netherlands is nonetheless at the centre of Europe’s gas market. A mixture of history (the European gas market was founded there) and forward planning, such as the construction of the Gate LNG import terminal at Rotterdam and a network of key import and export pipelines has established it as the continent’s most important natural trading hub.

Like most natural gas markets, it is a virtual trading point, meaning that it allows buyers and sellers to change ownership (‘Title’) of gas in the grid without having to deliver it physically. This virtual setup allows for a wide range of counterparties to be active, significantly deepening liquidity to the extent that each molecule of natural gas is likely to change hands around 20 times before being consumed.

Traders can trade any delivery window from spot products such as "within-day" and "day-ahead" out to full calendar years up to several years ahead. As the nearest-dated contract that can be traded without taking physical delivery of gas molecules, the so-called "front-month" product, a rolling product describing gas delivery during the next full month, has long attracted the bulk of future-dated TTF liquidity. AFI’s LNG quotes represent a quarterly average of the ICIS TTF front-month benchmark. The TTF index does not reflect the the delivered price of LNG fuel to ships. There will be significant mark-up costs which varies with e.g. drop-volume, distance to source and delivery mode.

Comments

No comments yet. Be the first to comment!